Stablecoins and the Fragmentation Trap: Why Orchestration Is the Missing Piece for Business Payments

Key takeaways:

- While stablecoins make moving money faster, cheaper, and more transparent, companies still need to solve for licensing, banking access, FX, compliance, and system integration.

- This leads to the fragmentation trap: the false belief that solving for technology challenges automatically addresses regulatory and business process challenges. Trying to solve this problem alone—stitching together wallets, on/off-ramps, compliance tools, and banking partners—creates fragmented operations, long launch timelines, and hidden risk.

- Orchestration platforms turn stablecoins from a promising tool into a usable stablecoin payments platform for businesses and payment providers. By unifying infrastructure, compliance, and operations into a single flow that dynamically routes transactions, businesses can actually realize the benefits of stablecoins without needing to rebuild the financial system themselves.

—

Stablecoins are entering their moment.

Not long ago, anything associated with crypto felt questionable, especially after high-profile fraud investigations like FTX. But that perception is shifting and the numbers show it, with stablecoins powering over $300 billion in real economic payments.

What’s changed is a combination of attitude and infrastructure. Businesses are more open to the category and the stablecoin infrastructure—APIs, compliance tooling, and access points—has matured.

At the same time, the value proposition is increasingly clear. The core benefits of stablecoins include faster settlement, lower costs, and full transparency. In some cases, they can reduce settlement costs by more than 75%.

So why wouldn’t every business just use stablecoins?

The answer, unfortunately, is because consumer expectations do not always match business reality.

Sending USDC wallet-to-wallet feels like sending a Venmo or e-transfer. It’s instant and global. But running a compliant, auditable, cross-border payment system is something else entirely.

That’s where things break down. And it’s where businesses fall into what we call the fragmentation trap.

How cross-border payments work—and where stablecoins fit

When you send money through traditional cross border payments, you’re not actually sending money from your bank to the recipient’s bank. In most cases, you’re instructing your bank to coordinate with a network of partners. One institution reaches out to another, which connects to another, until the funds are delivered locally.

On average, one to three intermediaries are involved, just to move your money from place to place, each taking a fee for their trouble.

From the user’s perspective, it feels simple and digital. But underneath, it’s a layered system of intermediaries, fees, and delayed settlement. At any given point, no single party has a complete, real-time view of where the money is.

Stablecoin payment rails change that model.

Instead of relying on a chain of institutions, the blockchain validates the transaction. The money itself is digital and moves digitally, eliminating the need for intermediaries. Stablecoin payment infrastructure also enables real-time tracking and provides confirmation that funds have arrived.

Stablecoins feel simple because they seem like an instant, peer-to-peer money network. But businesses don’t operate in a peer-to-peer context. They operate in a regulated environment with requirements that go far beyond sending money.

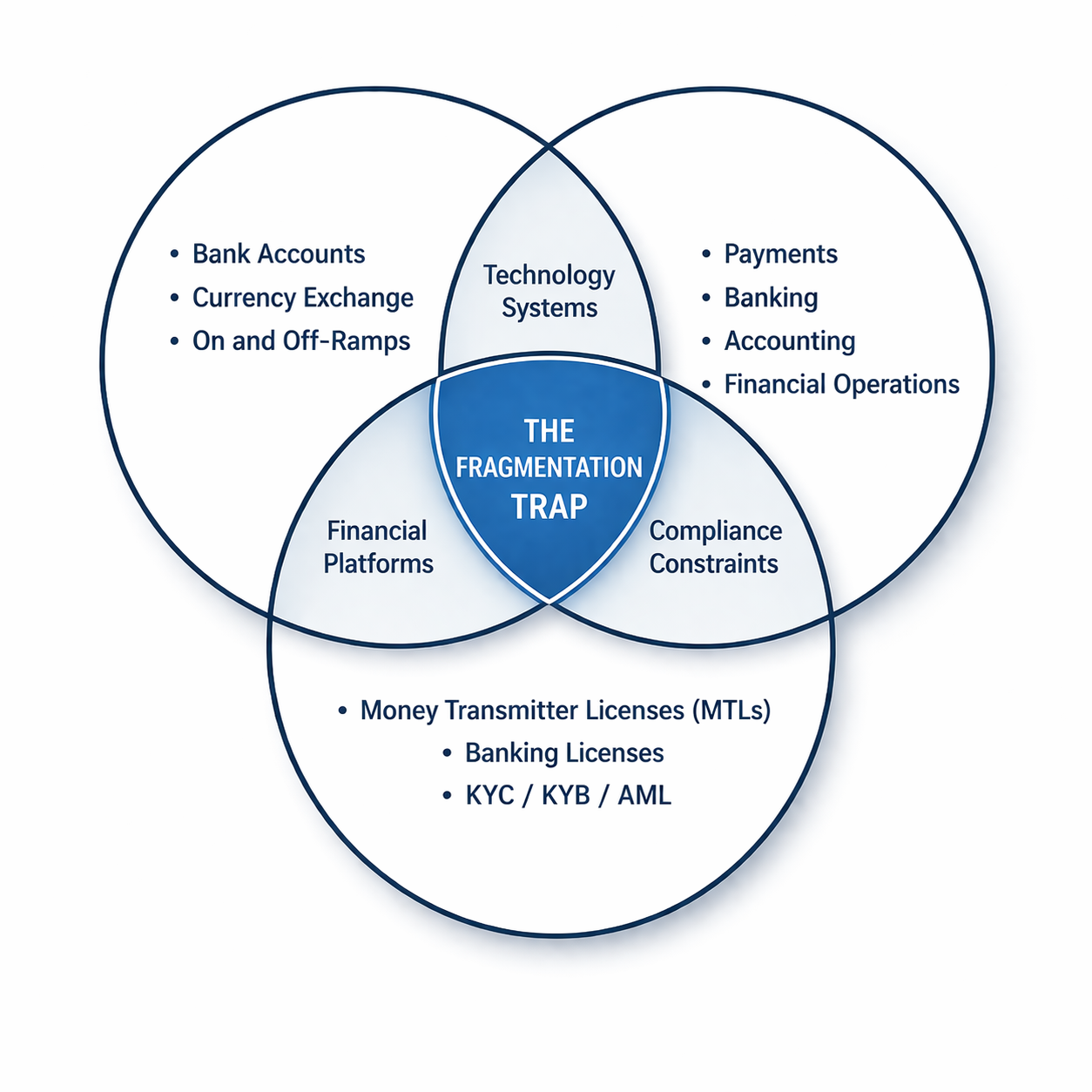

Understanding the fragmentation trap

The fragmentation trap begins with the misunderstanding that technical, process, and regulatory challenges can all be solved with a single innovation. Stablecoins solve the technical problem of moving value. They do not solve the regulatory, financial, or operational layers required to make that movement usable in a business context.

Those layers still need to come together.

You still need financial infrastructure like bank accounts, FX, and on/off-ramps for international payments. You still need operational systems for workflows, reconciliation, and reporting. And you still need to meet regulatory requirements like licensing, KYC, KYB, AML, and stablecoin compliance.

The challenge is that these systems don’t naturally connect.

So companies end up assembling them manually, connecting digital wallets, liquidity providers, compliance tools, and broader payments infrastructure partners. Each piece works on its own, but stitching them together creates the space for fragmentation.

How companies fall into the trap

The path into the trap is predictable.

A company decides to add stablecoin payments rails. They choose an asset like USDC, integrate a wallet provider, and enable basic send and receive functionality. Early progress feels fast.

Then the real requirements emerge:

- On/off ramps

- Licensing and business registration

- Liquidity

- FX coverage

- Bank relationships

- Payout partners

Individually, these all seem like solvable problems. But each step introduces a new dependency and a new opportunity for integration delays. Licensing requirements take time and vary by jurisdiction, for example. Banking access is not guaranteed. Regulatory expectations are inconsistent and often unclear. These are structural constraints within international payments infrastructure, not engineering challenges.

The turning point usually comes when the product is nearly ready, but a key corridor partner—for instance, a payout provider India—takes months to unlock. Not because of technical limitations, but because of regulatory approvals and partner constraints.

At that point, you’ve fallen into the trap without realizing it. You can solve the technical layer. But you cannot solve the system alone.

The missing piece: orchestration

Orchestration is when you leverage a third party platform that brings together financial infrastructure, operational systems, and compliance into a single, unified flow. That backend infrastructure also makes decisions in real time about how money should move—choosing the best rail, asset, and route for each transaction.

A simple way to think about orchestration versus fragmentation is the difference between a GPS system like Google Maps versus planning your own journey. If you try to go it alone, you might have access to a map, but you’ll have to think about construction, traffic, and optimal routes for distance versus time or scenery. Then you’ll have to think about which mode of transit to use, whether cabs, trains, buses, or driving. Or you can use Google Maps and it handles all of those pieces for you, simply giving you the best route to follow.

With payments orchestration, all necessary pieces are brought together for you so you can focus on integrating one system then going live in-market.

Instead of building the system, you’re operating on top of it.

Real-world example 1: A remittance app entering North America

For a remittance app to expand legally in the US or Canada, you need either your own licenses or a sponsor-bank model that allows you to operate under an existing framework. And that’s before you build a single payment rail or try to build the “stablecoin sandwich”.

This is where expansion strategies often break down—and where orchestration can help.

Here’s how it can go bad:

- Companies invest in product UX, only to discover that they cannot legally operate or access the banking system in the way they expected.

- Or they realize that even once they get compliant banking relationships, integrating stablecoins will be yet another challenge because they also have to plan for payout partners and FX systems.

Orchestration platforms like Cybrid address this by providing licensed infrastructure and sponsor-bank relationships. They also provide the APIs necessary to integrate stablecoin payment rails into your platform. Instead of becoming a money services business themselves or needing to rebuild custom rails, companies can operate within an existing framework and enter the market faster.

Real-world example 2: A payments platform adding stablecoin rails

Consider a regional business payments platform looking to improve cross-border performance for their customers. Their goal is straightforward: reduce settlement times, lower costs, and offer faster payouts. Stablecoins seem like a natural extension of their existing system.

Starting seems easy enough: integrating wallet infrastructure and enabling stablecoin transactions.

Then the fragmentation trap sets in with issues around sourcing on/off-ramps, liquidity, and integrating stablecoins flows into existing ledgers and reconciliation systems. And that’s all before the need to meet licensing and compliance requirements for new types of transactions.

In the end, the company is stuck with an ever-growing network of vendors and integrations, longer timelines, and increased operational overhead.

With an international payments orchestration layer from a platform like Cybrid in place, fiat and stablecoin flows are unified. Compliance and licensing are handled within the system. Liquidity and routing are handled within the platform. Integration into existing workflows from APIs becomes straightforward.

The outcome is what they originally expected: faster time to market, reduced complexity, and the ability to offer stablecoin-powered payments without changing their user experience.

Two ways to orchestrate

Once you recognize that orchestration is required, the next question is how to approach it.

In practice, there are two models.

Option 1: Managed approach

This is how most startups and mid-market companies operate. Instead of building and owning the underlying infrastructure, they use orchestration layer APIs that provide it. That includes licensing coverage, banking access, compliance systems, and connectivity to stablecoin rails.

The benefit here is speed and focus. You don’t need to become a regulated entity or build relationships with sponsor banks yourself. You can go to market faster and concentrate on your product and customer experience, rather than the underlying system.

Option 2: Self-managed approach

This is more common for banks, credit unions, and large fintechs that already have money transmitter licenses, banking relationships (or their own custody), and compliance teams in place. In this case, orchestration is still necessary—but it’s applied to coordinate stablecoin rails with existing infrastructure rather than an out-of-the-box solution.

The key point is that orchestration isn’t optional in either model. The difference is simply who owns the underlying pieces.

A system, not just a technology

Stablecoins are a powerful tool in financial services, but they are not a silver bullet.

The companies that win won’t be the ones that simply tell teams to “use stablecoins”. They’ll be the ones that integrate them into how their business actually operates.

Ready to move your business onto stablecoin rails?

Where technology meets money movement